Latest inflation figures

The 12 month CPI rate of inflation - the most widely used inflation measure - spiked up in January to 3% from 2.5% in December.

The rising cost of transport, food and non-alcoholic drinks was the biggest contributor to the rise, the highest CPI rate for 10 months.

Rises in private school fees, partly due to the addition of VAT, and a smaller than expected drop in air fares also fuelled the spike.

The biggest downward contributor came from housing and household services.

Industry experts are predicting that CPI could hit 3.7% by the autumn before subsiding.

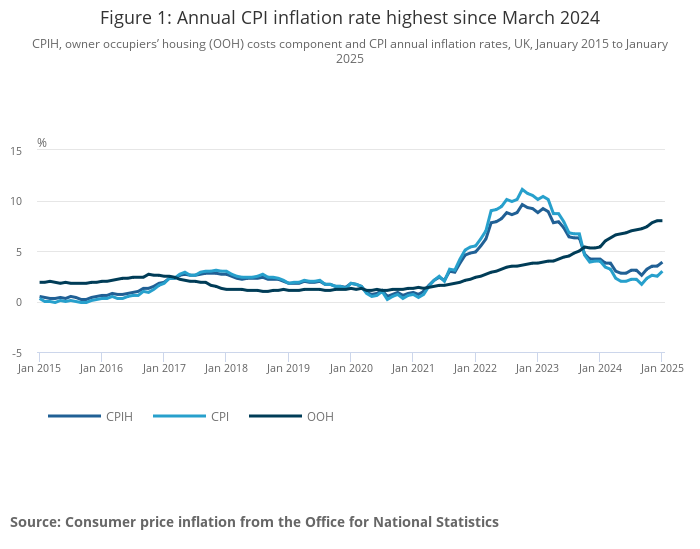

ONS said that the Consumer Prices Index (CPI) rose by 3.0% in the 12 months to January, up from 2.5% in the 12 months to December 2024.

The wider Consumer Prices Index, including owner occupiers' housing costs (CPIH), rose 3.9% in the 12 months to January, up from 3.5% in December 2024.

Core CPIH (excluding energy, food, alcohol and tobacco) rose 4.6% in the 12 months to January, up from 4.2% in December 2024 while the CPIH goods annual rate rose from 0.7% to 1.0%. The CPIH services annual rate rose from 5.4% to 5.8%.

Core CPI (excluding energy, food, alcohol and tobacco) rose by 3.7% in the 12 months to January, up from 3.2% in December 2024. The CPI goods annual rate rose from 0.7% to 1.0%, while the CPI services annual rate rose from 4.4% to 5.0%.

RPI, the older measure of inflation still in use in many sectors, rose to 3.6% from 3.5% the previous month.

Most experts said the inflation spike was disappointing but would be unlikely to change monetary policy yet.

Edward Smith, co-CIO at Rathbones, said: “The jump in core inflation back up to 3.7% and a return to 5% services inflation are not good news, especially when one considers that the Bank of England’s ‘decision maker panel’ survey indicates that firms expect to raise prices by about 4% over the coming year, and that survey has had a good predictive relationship with core inflation in the past.

"The upcoming impact of the rise in employers NICs, second round effects from public sector pay rises, and another large hike in the minimum wage all add to the uncertainty.”

James Lynch, investment manager at Aegon Asset Management, said: “A mixed bag for the inflation numbers out of the UK this morning. Headline Consumer Prices Index (CPI) came in higher than expected at 3.0% against 2.8% expected, but the services component ‘only’ came in at 5.0% against 5.1% expected.

“Overall, we believe the impact of this recent uptick in inflation is likely to be muted for investors. Defined Benefit pension schemes continue to be well hedged against this risk and for other investors we expect this increase to be temporary and expect disinflationary conditions to return into 2026 in the UK.”

"Services inflation, which represents a better gauge of domestically generated inflation than headline CPI, also accelerated from 4.4% to 5.0%. Although it was slightly softer than the 5.1% estimated by consensus."