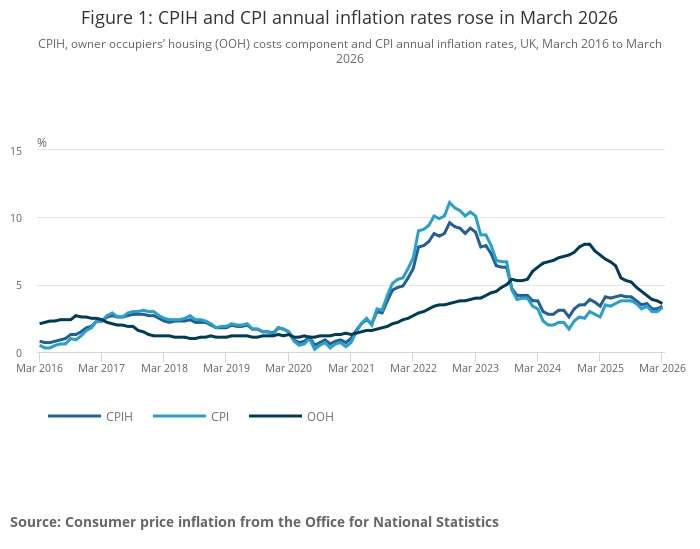

CPI inflation spiked up from 3% in February to 3.3% in March as the cost of fuel rose against a backdrop of conflict in the Middle East.

ONS said motor fuels made the largest upward contribution to the monthly change in both CPIH and CPI annual rates. Fuel costs, particularly diesel, have soared in recent months.

In contrast, clothing costs made the largest downward contribution, partially offsetting the rise.

The rise in CPI inflation will be bad news for the Bank of England which had recently seen inflationary pressures subside.

Many experts had expected worse inflation figures but, with uncertainty over the war in Iran, many believe the direction of inflation is hard to judge although further upward pressures are likely depending on the length and scale of the conflict.

Mike Ambery, retirement savings director at Standard Life plc, said: “Today’s inflation figure of 3.3% suggests that price pressures are starting to pick up against the backdrop of war in the Middle East, with the initial impact of volatile wholesale energy markets starting to feed through. However, this is unlikely to show the full picture.

“Energy prices have continued to rise into April, and their impact on the UK energy price cap - due to be updated in July - as well as on everyday costs like transport, food and other essentials, is still working its way through."

Kevin Brown, savings expert at Scottish Friendly, said: “March’s data reflects the early impact of recent energy price increases, with further inflationary pressure from conflict in the Middle East still to filter through. For many UK households, this is an unwelcome development at an already difficult time.

“Scottish Friendly’s Family Finance Tracker research, conducted before the recent conflict in the Middle East, showed six in 10 people do not believe the cost-of-living crisis is over, while two-thirds remain concerned about affording their regular outgoings over the next 12 months. Inflation is rising again, and sadly its impact on households’ financial confidence is nothing new."

Lindsay James, investment strategist at Quilter, said: "This morning’s inflation data showed CPI creeping back up to 3.3%, confirming that price pressures are re‑accelerating rather than fading away since the outbreak of the war in Iran. Markets had already moved to price in a quarter‑point Bank of England rate hike by the end of the summer but this data could add to pressure on the MPC to act.

"A rise in rates risks misdiagnosing the problem. This inflationary pulse is being driven by supply disruption, not excess demand. Higher interest rates will do nothing to increase the flow of oil or other goods from the Middle East. Financial markets are behaving as though the conflict is effectively over, with equity markets largely recovered and oil prices for future delivery falling from around $95 for June contracts to closer to $80 by year end.

"The physical market tells a very different story. Prices for immediate delivery into Europe are trading roughly $28 above benchmark levels, reflecting transport disruption rather than longer‑term demand."

Scott Gardner, investment strategist at JP Morgan Personal Investing, said: “It was always a question of how much UK inflation would rise after the war with Iran broke out. As this latest reading shows, we are starting to see the disruption in the Strait of Hormuz and the resulting spike in energy prices feed into elevated UK prices. The early inflationary signs are troubling, and this renewed increase in UK inflation will keep policymakers on alert over the short term."

ONS figures out today showed that Core CPIH (CPIH excluding energy, food, alcohol and tobacco) rose by 3.3% in the 12 months to March 2026, down from 3.4% in the 12 months to February. The CPIH goods annual rate rose from 1.6% to 2.1%, while the CPIH services annual rate rose from 4.2% to 4.3%.

RPI, the older measure of inflation, rose from 3.6% in February to 4.1% in March.

ends.