The Financial Services Compensation Scheme (FSCS) has declared Glasgow-based Atlantic Investors (Scotland) Ltd (FRN: 182565) as failed.

Fast-growing Financial Planning and wealth management group Loyal North has completed the acquisition of New Malden, Surrey-based Whitman Fry Wealth Management Ltd for an undisclosed amount.

Frenkel Topping, the specialist advice firm focusing on personal injury and clinical negligence cases, has acquired Chester-based cost consultants North West Law Services Limited (NWL) for £2.75m and revealed that profits for 2023 climbed by almost a third.

Pensions consultancy LCP is calling for a ‘magnetic pensions’ strategy to help tackle a leap in small pension pots, estimated to be increasing at 2m a year.

The FCA is keeping a close eye on an ‘uptick’ in overseas firms trying to establish an operation in the UK but keeping senior staff overseas.

Insurance and savings trade body the ABI has warned the Department for Work and Pensions (DWP) that a public pensions 'consolidator' must avoid undermining the DB scheme buyout market.

Fintech Twenty7tec has launched a web-based practice management and CRM solution for financial advisers.

Pension scammers are acting with impunity and few have ever been held to account, according to industry body The Pension Scams Industry Group (PSIG).

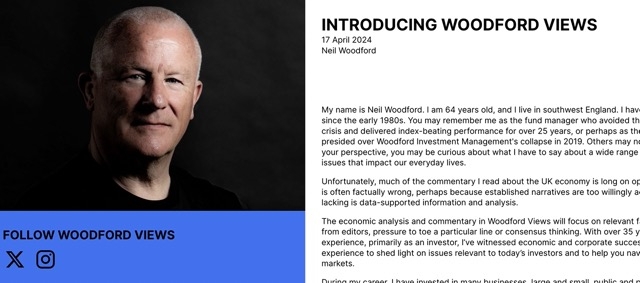

“I am neither hero nor villain,” wrote Neil Woodford for the launch of his new website Woodford Views, less than a week after the FCA issued him with a warning notice.

Financial Planning trade body the Personal Finance Society (PFS) is to sponsor the 2024 NextGen Planners conference.