Net retail sales recorded inflows of £2.4bn in February, a substantial increase on the £662m recorded in January and marking the fourth consecutive month of inflows.

It was their highest level since the £3.2bn recorded in May 2025.

Data published by the Investment Association showed a higher inflow into actively managed funds at £1.5bn compared with index trackers at £890m.

The IA said UK investors continued to favour fixed income funds over allocating to equity sectors.

In the first two months the year it said investors were facing into relatively resilient economic conditions with inflation in the UK continuing to fall and generally positive equity market performance.

Funds under management and net sales – February 2026

| Funds Under Management | Net Retail Sales | Net Institutional Sales |

February 2026 | £1.70 trillion | £2.4 billion | -£1.1 billion |

February 2025 | £1.51 trillion | -£144 million | -£2.6 billion |

Source: Investment Association

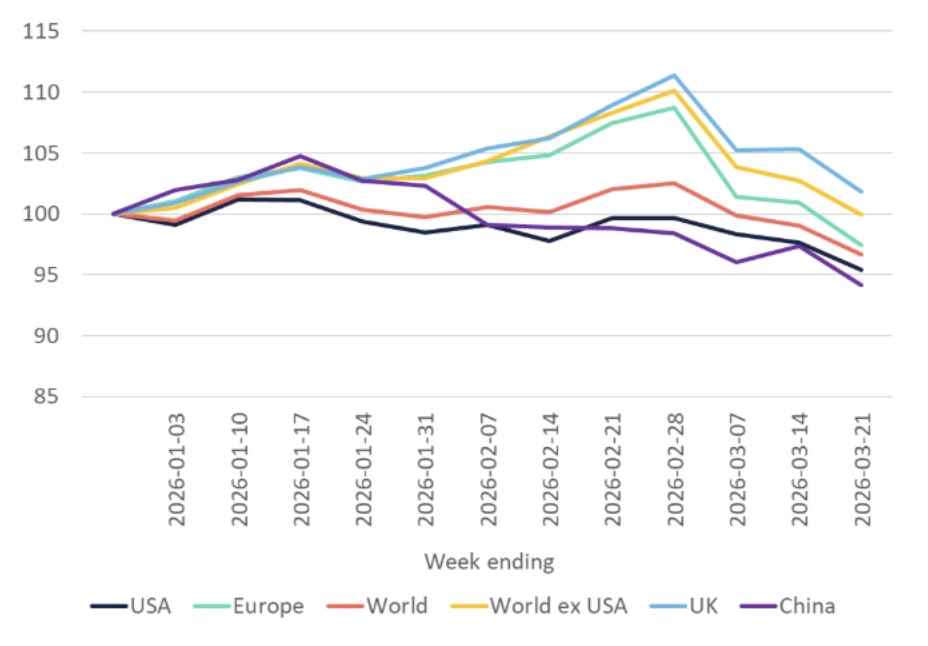

However, the reporting period preceded the recent conflict in the Middle East and the spike in oil prices following the closing of the Strait of Hormuz, which means that the outlook for investors in April is far more uncertain.

In February, Equity funds continued to see overall outflows of £465m, though UK investor demand varied significantly by region and sector. North American equity funds attracted sales of £417m, the highest since April 2025 (£966m), with continued inflows into North American tracker funds (£554m).

However, global equity outflows widened to £808m at the same time as global trackers posted outflows of £236m, following £479m of inflows in January.

The five best-selling Investment Association sectors for February 2026 were:

- Short Term Money Market saw net retail inflows of £600m

- North America saw net retail inflows of £443.9m

- Volatility Managed saw net retail inflows of £306m

- Targeted Absolute Return saw net retail inflows of £255.9m

- Global Equity Income saw net retail inflows of £204m

The worst-selling Investment Association sector in February 2026 was Global, which experienced outflows of £838.9m.

Despite some caution towards equities, other asset classes remained in demand, the IA said. Fixed income recorded inflows of £824m as investors continued to favour lower-risk allocations.

The Global Emerging Market Bonds – Local Currency sector posted inflows for nine of the last 12 months, suggesting that despite elevated geopolitical risks, it continues to benefit from demand for diversification and a weaker dollar. Similarly, money market funds saw continued demand (£551m) as investors continued focusing on managing risk.

Miranda Seath, director, market insight & fund sectors at the IA, said: “Investor confidence has been gradually rebuilding. While some hesitancy towards equities remains, investors are selectively re-entering the US market through equity trackers, whilst continuing to allocate to European and global emerging market equity funds. Fixed income remains in favour as investors continue to manage risk. Money market funds continued to attract inflows, which also reflects a more risk-off positioning.”

Looking ahead, she said investors “will be watching geopolitical developments, including the evolving situation in the Middle East and its potential implications for energy prices and inflation.

“However, investing remains a long-term proposition, and it is important that short-term volatility does not drive knee-jerk decisions.”