The requirement to seek financial advice has been identified as among the main reasons why people have made official complaints about pension freedoms.

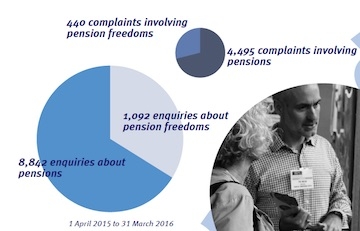

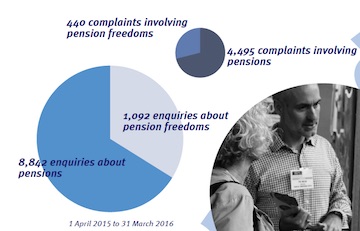

The Financial Ombudsman Service revealed today it received 440 complaints and 1,000 enquiries about pension freedoms in the first year after they were implemented.

Delays (24%) and the requirement to seek financial advice (15% ) were the two most commons reasons why people complained.

Ombudsman Mr Miller said: “We’ve heard from people trying to access their pension who are unhappy they’ll have to pay for advice.

“Some tell us they’re struggling to find an adviser who’s willing to give them advice, meaning their pension provider won’t let them access their pension.”

The main issues involved in complaints about pension freedoms were:

• administration 14%

• annuities 13%

• can't access pension 9.5%

• requirement to get financial advice 15%

• information given about pension 10.5%

• exit fees 5%

• delays 24%

• quality of advice 3.5%

• provider doesn't offer preferred pension option 5%

• other problem 0.5%

The main issues involved in enquiries about pension freedoms were:

• administration 19%

• annuities 6.5%

• can't access pension 8.5%

• requirement to get financial advice 11%

• information given about pension 8%

• exit fees 3%

• delays 41.5%

• quality of advice 2%

• occupational pension scheme benefits 0.5%

Mr Miller said: “The government’s figures suggest around a quarter of a million people accessed their pensions in the first year of the new rules. During that time we’ve dealt with around 1,000 enquiries and around 400 complaints.

“That suggests that so far, only a fraction of people who’ve used the freedoms have encountered problems – or at least, not things their pension provider hasn’t put right in a way they’re satisfied with.

“From our conversations with pension providers, we know there’s been a lot of work behind the scenes to make sure they’ve got the right resources in the right places – particularly to deal with the initial demand they anticipated after the changes came into effect. But inevitably – and providers have been upfront about this – delays have been an issue.”

Source: All charts above courtesy of FOS report

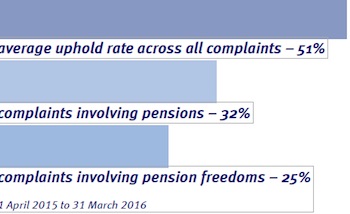

A third of pensions complaints in general have involved administration but that is currently slightly lower for the freedoms.

Mr Miller said: “A fair number of the complaints we’re seeing involve general administration and customer service issues. Pensions are a complex area, and consumers and providers have all had to navigate the new freedoms. So inevitably there’s been scope for misunderstandings and mix-ups.

“For example, the rules don’t require pension providers to offer all the different types of flexibilities. Sometimes providers get their messages wrong. Sometimes customers are simply frustrated to find they’ll have to go elsewhere to get the specific arrangement they want. Both these scenarios can lead to complaints if things aren’t clarified quickly.”