Fund manager and platform provider Fidelity is to implement a radical shift in the way it charges fund management fees, cutting annual management fees and moving towards performance-based charging.

The US-owned company says the move is a “fundamental” change and is in response to recent focus on the value of active fund management, a move towards improving client interests and the transparency of charging structures, some of these influenced by the imminent arrival of the MiFID II changes. The recent FCA Asset Management Review, which highlighted weak price competition between fund managers and confusing and high charging, was also a factor in influencing Fidelity to make changes to its charging structure.

The company said: “In response to the growing debate around the value of active fund management, the industry’s alignment with client interests and the transparency of charging structures, Fidelity International believes that now is the time to make a fundamental change in how it charges for its services.”

Fidelity will introduce a new variable management fee model across its active funds for all clients around the world. The company says that this will mean a reduction of the annual management fee and a change to a variable management fee that is “symmetrically linked” to fund performance.

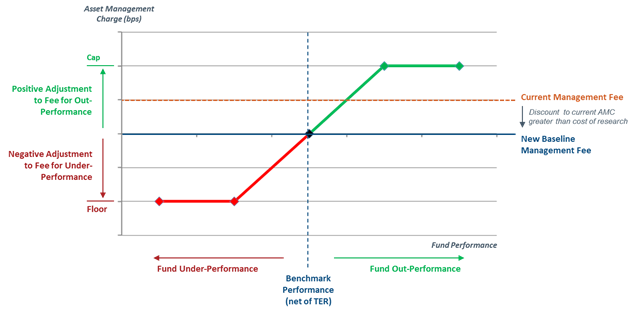

The variable management fee will operate on sliding scale and acts as a two-way sharing of risk and return - also known as a 'fulcrum fee’, says Fidelity. If a fund outperforms net of fees the company will share in the upside. If clients experience only benchmark level performance or below, they will see lower fee levels. The actual fee that clients will pay will sit within a range and will be subject to a pre-determined cap (maximum) and floor (minimum).

How Fidelity's 'Fulcrum Fee' will work

Brian Conroy, president of Fidelity, said: “We want to demonstrate real commitment to our active management capability. We will move away from a flat fee model and get paid according to how well we do for our clients. These changes will more closely align the performance of our business with the performance of our clients’ portfolios and deliver what we believe clients and regulators are looking for. Our fee structure will give back for underperformance of the benchmark, whereas others do not.”

“We are also announcing today our position with regard to MiFID II regulations and third-party research. We fully support the objective of the regulations but believe the debate has focused singularly on which model asset managers will use to pay for external research, rather than the total cost of asset management services and the value they deliver. In addition, the global nature of our business, both in terms of our clients and their access to our internal global research platform, means we need to apply a consistent model across our business.

“With this in mind, we have decided to adopt the CSA-RPA model for procuring third-party research but the reduction of our base management fee will exceed and offset the allocated client charge for this research. We believe that the CSA-RPA model is a flexible, transparent and globally consistent way to access the range of external inputs required to support our active management process.”