Total assets under management rose 19.8% year-on-year to £14.78bn for investment manager Tatton Asset Management for the six months ended 30 September.

Global Financial Planning professional body The Financial Planning Standards Board has added a new award recognising individuals for their outstanding contributions to the profession.

Advised customers increased 10% year-on-year to 159,256 at platform and SIPP provider AJ Bell for the year ending 30 September.

Investment provider Hargreaves Lansdown has reported client numbers rose by 8,000 to 1.812m in the latest quarter, according to a trading update issued today.

Accountancy professional body ICAEW has partnered with technology firm RQ to launch an online platform enabling Chartered Accountants and Financial Planners to refer clients.

Financial Planner and accountancy firm Old Mill has appointed Financial Planner and digital advice specialist Hugh Johnson to its wealth management team.

Aviva-owned wealth manager and Financial Planner Succession Wealth has added two new executives to expand its senior leadership team.

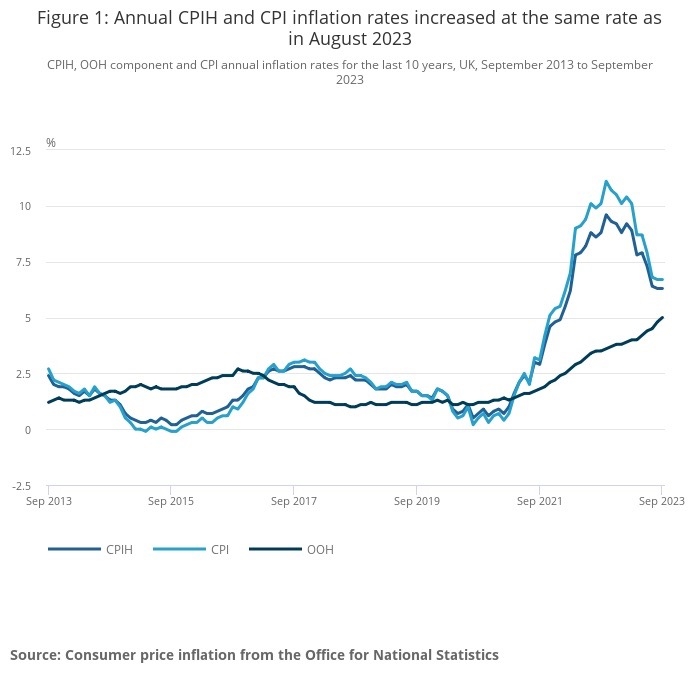

Retirees are set to receive an 8.5% increase to their State Pension from April next year as CPI inflation held steady at 6.7% for the year ending September.

Quilter saw third quarter core business net inflows of just £1 million compared to net inflows of £324 million in the corresponding period of 2022 amid "challenging" market conditions.

The Consumer Prices Index rate of inflation held steady at 6.7% in September, disappointing some commentators.