Platform Transact has reported total Funds Under Direction for Q4 rose by nearly £5bn year on year to hit a record £54.9bn, according to figures released today by parent company Integrafin Holdings plc (IHP).

Wealth manager St James's Place (SJP) - which announced a major overhaul of charges today - has reported gross and net inflows down in the three months ended September.

The Financial Services Compensation Scheme, the government back financial safety-net scheme, has appointed a new interim CEO today but says a new permanent CEO will not be appointed until after April.

Newly-launched adviser firm MRW Group has acquired three financial advisory firms with the help of funding from OakNorth, a bank for entrepreneurs.

Wealth manager St James’s Place announced today that its much-criticised charging structure will be full revamped by the second half of 2025.

After intense pressure from several quarters, wealth manager St James's Place said today that it would scrap most exit charges in a major overhaul due to be implemented in the second half of 2025.

Expanding national advice firm Foster Denovo Group has reported assets under management in 2022 rose to £1.2bn, up 9% on 2021.

Nearly three-quarters of people have been targeted by scams in the past year with a majority of approaches online, according to new figures published today.

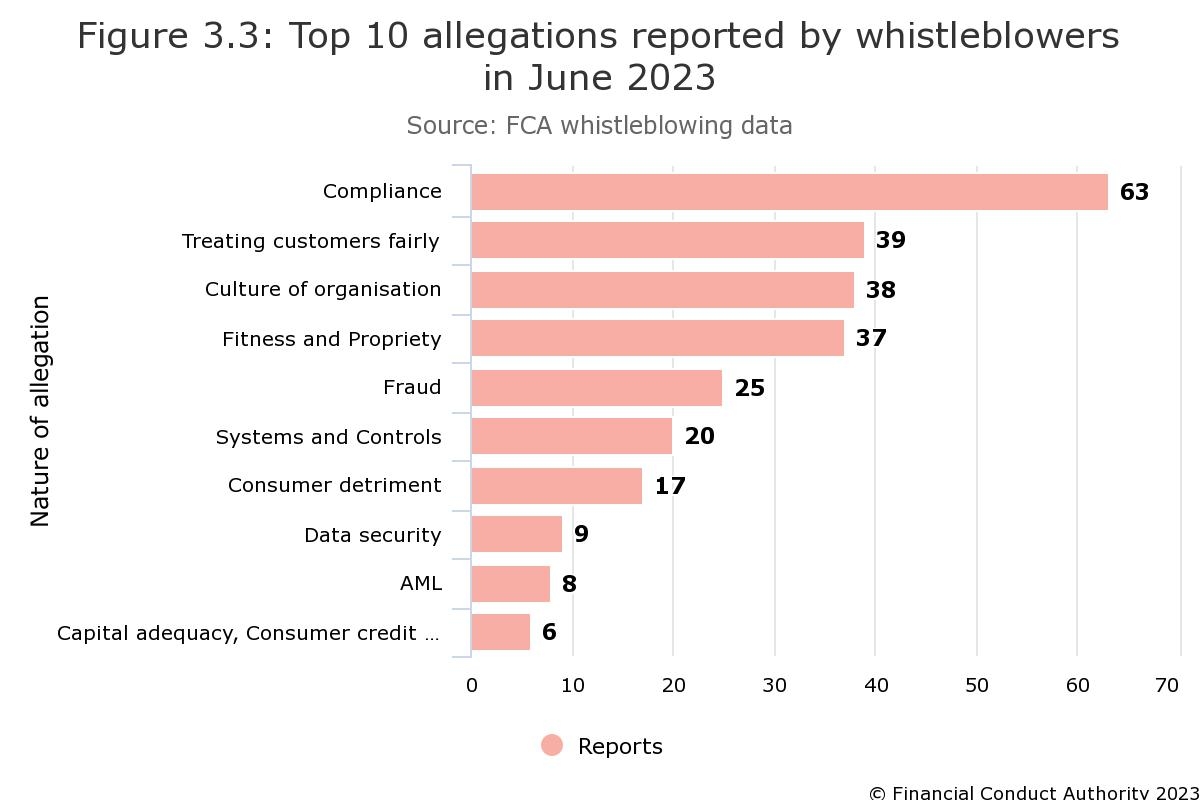

‘Compliance’ was the top reason for whistleblowers to complain to the FCA in June, with 63 reports being made to the regulator about the issue during the month.

Cheshire-based Financial Planner Equilibrium has hit a landmark total of £1m in donations to good causes through its charitable giving arm The Equilibrium Foundation.