Mary Stewart of Sipps specialist Hornbuckle Mitchell focuses on the new rules on flexible pension drawdown and how the market is evolving as a result. She looks at the opportunities for planners and some of the hurdles to be overcome.

New rules creating flexible drawdown as a way to take pension benefits have opened up a host of new Financial Planning opportunities. For the first time, retirees have been given the green light to take as much as they want, when they want.

Visions of millions of people gleefully emptying their pension pots overnight can be dispelled. One reason is that flexible drawdown will be restricted only to those who can meet the Minimum Income Requirement of at least £20,000 a year of guaranteed income from state pension, final salary schemes and lifetime annuities.

Estimates suggest that of the 12.5 million people aged 55 to 75, between 5 per cent and 8 per cent will have the required level of secured income. And of those, only about one in five – perhaps 200,000 currently – have sufficient defined contribution pension from which to take flexible drawdown.

Even the relatively few people who could strip out the fund are unlikely to do so. Pension income is subject to income tax so most will aim to minimise their tax liabilities by taking the money in smaller regular payments. By only crystallising the amount of pension fund needed, death benefits can also be maximised.

Flexible drawdown may not be for everyone, but those relatively wealthy people it will attract are the natural clients of the professional Financial Planner precisely because they are looking for intelligent strategies for maintaining wealth and generating income. It is also likely that the numbers looking to use flexible drawdown will increase over time as the number and size of defined contribution pension pots grows.

It should not be seen solely as the preserve of the High Net Worth investor, however. In many cases it will be useful for people retiring on a good level of final income after long careers. Many will be civil servants and white collar public sector workers who would prefer total freedom when accessing the funds in top-up money purchase pensions built up on the side.

The new rules that created flexible drawdown at the start of this tax year also created capped drawdown. As the name suggests, capped drawdown imposes a limit on the amount of income that can be taken from the fund. There are potentially far greater numbers who could use capped drawdown than flexible – between 600,000-700,000 people aged 55-75 are already in drawdown or could use capped, according to research from the Pensions Policy Institute earlier this year.

Drawdown appeals to investors who want to keep control of their pension funds and the associated income for longer in retirement. It can tie in with staged retirement strategies that are becoming more common among modern retirees and which give income flexibility. At times like the present when the health of the global financial system is in question, drawdown can provide a way to ‘wait and see’ option until stability returns.

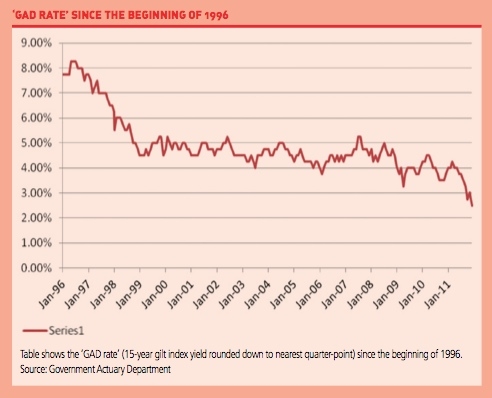

As the chart shows, since drawdown was introduced more than 15 years ago, the GAD rate has been on a downward trend. The credit crunch has accelerated this fall from more than 5 per cent in 2007 to 2.5 per cent in December, its lowest level since drawdown was introduced more than 15 years ago.Unfortunately, the economic crisis continues to impact on those reaching drawdown reviews or thinking of starting capped drawdown for the first time. Demand for government gilts has shot up through the troubles, pushing up prices and reducing the yields available. The return on the 15-year gilt index – often referred to as the ‘GAD rate’ is one of the variables used when calculating the maximum that can be withdrawn under capped drawdown.

The table shows the ‘GAD rate’ (15- year gilt index yield rounded down to nearest quarter-point) since the beginning of 1996.

The low GAD rate is not the only issue facing drawdown investors. When the new rules were introduced in April 2011, they were accompanied by a tightening in the drawdown limits. Since 2006 drawdown investors aged up to 75 were able to take up to 120 per cent of the basis figure – roughly equivalent to a single life annuity return – published in Government Actuary’s Department drawdown tables. Since April this has been reduced to 100 per cent plus the tables themselves were revised to make them slightly less generous.

In March 2011 when the GAD rate was 4.25 per cent, a 65 year old man could take a maximum of £84 per £1,000 of pension fund each year, and a similarly aged woman could take £78. The April changes, plus the fall in the GAD rate to 2.5 per cent, meant the equivalent figures in December had fallen to only £56 for the man and £53 for the woman.

Some retirees who entered drawdown five years ago, perhaps drawn in by the new rules introduced at A-Day, who opted for maximum income will, we believe, be facing income falls of up to 50 per cent due to the combination of tighter income limits and depressed asset values.

The severity of the impact in such a short time has galvanised calls for change within the industry. In a recent poll by a major Sipp provider, more than 97 per cent of advisers wanted a change with the majority calling for the link between gilt yields and maximum drawdown amounts to be replaced by a simpler system. The government is sticking to its new rules, believing the current conditions are temporary and presumably confident the limits will stop drawdown investors depleting their funds too quickly.

This is a major concern of governments who want to stop people falling back on state help in the future and is the reasoning behind the Minimum Income Requirement for entering flexible drawdown. PPI research earlier this year showed the danger.

It suggested that a 60 year old woman expected to live to 89, who takes the maximum capped drawdown from a £123,500 pension fund, has a 36 per cent chance of depleting the fund before her death. If she took only half of the maximum withdrawal, there was still a 2 per cent chance the fund would run out before death. However, the flipside was that even if she was taking the maximum there was a 33 per cent chance of the fund value doubling by age 89.

If anything, the range of possible outcomes for those using income drawdown – whether flexible or capped – proves little more than the massive importance of professional advice to help intelligently manage the process over time. As increasing numbers of baby boomers reach retirement, there should be no shortage of opportunities to show the value of Financial Planning.

Having had a year to prepare, the numbers entering flexible drawdown are going to start increasing from April 2012 onwards. There is scope for Financial Planners to help these clients maximise their contributions while they can, making best use of the carry forward rules and pension input periods to pay in extra and receive tax relief while they can.

Partial flexible drawdown is likely to become a popular strategy for those meeting the MIR. The new rules have introduced a 55 per cent tax charge on residual pension paid to beneficiaries as a lump sum death benefit, compared to a previous rate of 35 per cent for 55 to 75 year olds. However the tax is avoided, up to age 75, where the fund is uncrystallised. The message is that clients in early retirement should not crystallise unless they need to, and we expect many will use partial flexible drawdown to take only what they need.

Low gilt yields and tighter income restrictions may not be helping its cause, but capped drawdown is going to continue as a mainstay of retirement planning, particularly in early retirement when people in good health want to keep their options open.Where the squeeze on income is just too tight, Financial Planners should consider Scheme Pension via a Sipp as an alternative. This can operate as a self- invested arrangement but the income limits avoid GAD restrictions and are instead set by an actuary based on the scheme member’s own circumstances including their health. Financial Planners then work with clients to assess risk appetite and investment strategies in order to determine the level of income to take.

The income potential is greater than capped drawdown would allow – the 65-year-old man mentioned above limited to £56 a year per £1,000 of pension under capped drawdown could take 40 per cent more (£78.35) under scheme pension if in good health, rising to 77 per cent more (£99.17) if in very poor health.

Financial Planners need to be familiar with the pros and cons of scheme pension as they are with drawdown and annuity options. No-one knows for sure what will happen to investment returns, annuity rates or gilt yields in a month, a year or a decade. But today’s rules create some compelling Financial Planning opportunities that clients will be keen to discuss.